CNX Sustainable Business Model

Grounded in our Appalachia First vision and supported by our Core Values, CNX’s Sustainable Business Model (SBM) and initiatives position us as a leader in the environmental, social, and governance aspects of the energy industry.

Grounded in our Appalachia First vision and supported by our Core Values, CNX’s Sustainable Business Model (SBM) and initiatives position us as a leader in the environmental, social, and governance aspects of the energy industry.

Our legacy of innovation and forward-thinking has kept us ahead of the curve on crucial issues in our sector, region, and the world. Sustainability is central to our strategy for value creation and our methodical focus on prudent capital allocation. Our strategy is to foster a SBM that applies the nonreplicable advantages of our structural cost advantages resulting from integrated upstream and midstream business lines and a “stacked pay” acreage position in one of the world’s most prolific, lowest cost, and lowest methane intensity natural gas basins. Our unique, ultra-low carbon intensity premium products such as Remediated Mine Gas (RMG), coupled with our industry leading environmental practices, including the first-of-its-kind Radical Transparency initiative in collaboration with the Commonwealth of Pennsylvania, protect and advance the company’s core business license to operate while also ensuring CNX remains at the forefront of emerging market opportunities for low carbon intensity products.

These advantages drive our Sustainable Business Model, consistent generation of free cash flow (FCF) per share, and present a differentiated upside versus our Appalachian peers. When coupled with our clinical capital allocation philosophy, we are positioned to deliver substantial intrinsic value creation per share for our owners for years to come.

Competitive Moats

Our non-replicable advantages provide a wide competitive moat that allows us to generate regular and continued, substantial FCF.

Integrated Midstream

CNX owns and operates natural gas gathering pipelines, along with a number of natural gas processing facilities. Our integrated upstream and midstream business provides a competitive cost advantage, as reflected in our low operating costs, and allows us to provide natural gas gathering services to third parties, affording us significant flexibility in our operations. We have developed a processing portfolio to support produced volumes from our wet gas production areas and have the operational and contractual flexibility to convert a portion of currently processed wet gas volumes to be marketed as dry gas volumes, or vice-versa, as economically appropriate. We also have the advantage of natural gas production from lower Btu wells in close proximity to higher Btu wells. In the absence of an integrated midstream, low and high Btu natural gas may need additional processing to meet downstream pipeline specifications-a costly process, routinely incurred by our competitors. The geographic proximity and interconnected gathering system servicing these wells allow CNX to blend this gas together and, in some cases, eliminate the need for the costly processing of natural gas that does not meet pipeline specification. This allows us more flexibility in bringing wells online at qualities that meet interstate pipeline specifications. An integrated midstream operation allows us the flexibility to free flow a significant portion of early production volume while utilizing the energy from the wellbore. Free flowing this production can significantly reduce compression costs and emissions incurred during the early phase of well production.

We continue to make substantial investments in water pipeline infrastructure with a significant network of water lines. Transporting water through pipelines reduces the risks and carbon footprint associated with transportation by truck and minimizes our impact on the community and environment in Appalachia. CNX works to develop solutions that coincide with our midstream operations to offer natural gas gathering and water delivery solutions in one package to third parties.

Stacked Pay (Utica and Marcellus)

CNX has a significant inventory acreage position that was built over 160 years, much of which is unique multi-formation acreage. This non-replicable asset base allows for stacked pay development of the Marcellus and Utica shales that drives superior financial returns through economies of scale, greater flexibility, and a reduced footprint. From an environmental perspective, stacked pay development limits earth disturbance and associated emissions from construction of additional well pads and infrastructure, reduces excess hauling traffic from local highways, and minimizes secondary fuel consumption. This type of development reduces capital investment by reusing pads and our midstream and water infrastructure.

It also reduces cycle times and reduces gathering and processing fees as we blend our gas-as described in the Integrated Midstream section above. Stacked pay development presents an unparalleled opportunity to lead the development of, what we believe are, one of the world’s two most prolific natural gas basins.

Low Carbon Intensity Premium Products

We generate FCF through the monetization of environmental attributes associated with RMG from our waste methane capture operations in Virginia and Pennsylvania. In the near term, we expect to continue to monetize similar levels of environmental attributes into the low carbon electricity generation market via the Pennsylvania Alternative Energy Portfolio Standard (AEPS) program. Longer term, we will continue to focus on expanding our premium, low carbon intensity RMG product into other markets – such as manufacturing, data centers, transportation, commercial heat, and aviation – that are seeking to decarbonize their supply chains.

We will also continue to pursue emerging regulatory compliance programs that further validate the intrinsic positive economic and environmental value of waste methane capture. For example, RMG has been included in the Department of Energy’s Greenhouse gases, Regulated Emissions, and Energy use in Technologies (GREET) life cycle assessment model, the 45Z CF GREET model as alternative natural gas, as well as the 45V Hydrogen Production Tax Credit final rule. These developments represent the first federal recognitions of RMG’s inherent value and provide important validation and entry into other emerging market opportunities for our low carbon intensity premium product.

In addition, the company continues to advance its AutoSep Technologies and CNG/LNG business opportunities, transitioning from the technology development and validation phases into the early commercialization phase. We expect to see their positive impact to FCF unfold in the years ahead.

Radical Transparency

As a key factor in the CNX Sustainable Business Model, successful community engagement starts with understanding how we can better collaborate with our stakeholders through transparency, dialogue, and active listening. CNX leads the industry with its historic commitment to this transparency through operational disclosures in connection with its Radical Transparency program, a collaborative effort between CNX and Pennsylvania Governor Josh Shapiro that allows the Pennsylvania Department of Environmental Protection (DEP) to conduct the most intensive independent study of unconventional natural gas wells in the nation. This comprehensive program-which publicly discloses air quality monitoring in real time, and provides information on water quality monitoring, additive disclosures, waste metrics and every Notice of Violation we receive -ensures local families, neighbors, and the public at large have a full understanding of the natural gas industry and its critical role in the environment and economy.

This unprecedented brand of transparency is good for resident and worker health, for economic development, for energy security, for the environment, and for community investment, and is critical to future public policy in the Commonwealth of Pennsylvania and the industry’s long-term license to operate.

Results

Our non-replicable competitive moats lead to the following advantages.

Low Methane Intensity

The Appalachian Basin is the lowest methane emission intensity basin in the United States, and CNX is a leader in driving meaningful methane emission reductions in the basin. We have made significant reductions since 2020 and intend to continue our methane management initiatives-even as we expand our operational footprint. Executive compensation is tied to methane intensity targets and has been since 2021. CNX uses cutting-edge data management tools and technology to further these efforts along with a collaborative Emission Reduction Task Force including members from operational, environmental, engineering, and data management teams. Furthermore, we capture waste methane from other industries-far more than we emit in our own operations-for processing, compression, and transport to market.

Low Cost and Low Capital Intensity Operations

Our all-in operating cost structure is the among the lowest in the Appalachian Basin, allowing the company to make long-term investments that generate high rates of return.

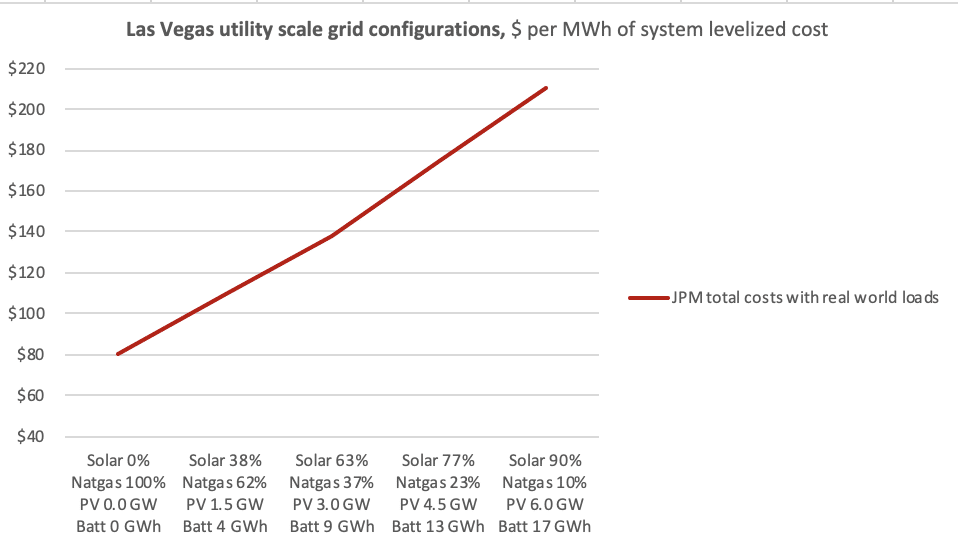

When compared to other energy sources, natural gas provides more affordable electricity than either solar photovoltaics (PV) or onshore wind in Pennsylvania. While the future of subsidies in the United States is uncertain, they are the only way wind and solar can compete with natural gas, but they force ratepayers to foot the bill in the form of higher taxes-paying the government instead of the utility. Further, the flexibility and dispatchability of natural gas is unmatched compared to intermittent wind and solar. Our world is experiencing growth like never before, requiring energy sources that can meet and sustain unprecedented levels of energy demand. The Appalachian Basin is one of the largest, most efficient, environmentally sustainable and cost-effective sources of natural gas in the world.

Even in a sunny place like Las Vegas, the costs (considering real world loads) are $130 per MWh higher using 90% solar power rather than 100% natural gas. (This excludes subsidies since someone is paying for them)

Consistent Free Cash Flow Generation

Our business continuously generates significant free cash flow (FCF) year after year, and we prioritize injecting that cash flow back into our business. Between 2020-2025, CNX generated $5.6 billion of net cash provided by operating activities, which resulted in $2.9 billion of FCF. In 2025 alone, the company generated $1.0 billion of net cash provided by operating activities, which resulted in an annual FCF of $646 million. Through the fourth quarter of 2025, CNX delivered 24 consecutive quarters of positive FCF, which has enabled the company to invest in our people and communities, reduce debt, and retire shares.

Capital Allocation Philosophy

We prioritize injecting free cash flow back into our business by investing in our people, assets, communities, and returning capital to our shareholders and debtholders.

Investing in our People and our Assets

We view investments in our team as high rate-of-return, value creation opportunities. A key priority of free cash flow allocation under our Sustainable Business Model is to invest in our employees. We embrace meritocracy. This means we pay for performance and Excellence in our daily work. We pay well as we perform well. We will continue to invest in our talented workforce to improve on our region-leading compensation profile.

We make significant annual capital investments in our operational assets based on a detailed review of risk adjusted rates of return. Our ‘follow the math’ philosophy means we invest in the highest return projects first, including our stacked pay Marcellus and Utica opportunities, as well as our integrated upstream and midstream infrastructure. In 2025, we invested $495 million of capital spending in our assets. This capital program resulted in the development of 625 Bcfe of reserves, representing a 1.0x proved developed replacement ratio, and bringing the total proved developed reserves at year-end 2025 to 7.0 Tcfe after adjusting for asset sales, price, production, and revisions. Finding and development costs for this activity, when including midstream and water infrastructure investments, were $0.62 per Mcfe. The ability to efficiently develop and replace our producing reserves year after year, even in low commodity price environments, is core to the creation of long-term, per-share value.

On January 27, 2025, we completed the strategic bolt-on acquisition of the natural gas upstream and associated midstream business of Apex Energy II, LLC, for total cash consideration of $518 million. This transaction expands our existing stacked Marcellus and Utica undeveloped leasehold in the CPA region and provides an existing infrastructure footprint that can be leveraged for future development, underscoring our confidence in the opportunities that have been unlocked from pioneering development in this region.

Investing In Our Communities

CNX has a long-standing and special relationship with the communities and people in our region. We have called Appalachia home for 160 years. The people and families within our walls and living in our operational footprint are one and the same. Over the years, we have become increasingly concerned that many of our friends and neighbors are denied access to economic opportunities in energy and manufacturing that represent a realistic path to the middle class. Our Appalachia First 2.0 vision sharpens our focus on hyper-local impact by meeting our communities where they are. We’re aligning our investments to create shareholder value while also supporting the needs of those who live and work in the region. We believe those two goals are inextricably linked.

The CNX Foundation invests in community initiatives aligned with its micro-Tangible, lmpactful, Local (micro-TIL) focus. This approach directs targeted investments to high-impact, community-identified needs in our operating area, directly targeting individuals and entities most in need. At CNX, community investment is more than a financial commitment. We strive to enhance our communities by lending our time and talent to organizations across the region. Doing so creates a virtuous circle of investment in our local communities that grows the region’s best-in-class workforce and pays dividends to CNX and the industry over the long term.

Returning Capital to Shareholders and Debtholders

We continue to view share repurchases as a compelling capital allocation opportunity, creating long term per share value for our owners. Since the peak share count in the third quarter of 2020, CNX has repurchased approximately 37% of our shares outstanding-98 million shares for $1.9 billion1-which equates to an average repurchase price of $19.27 per share. We believe that our share repurchase program provides an opportunity to create incredible value for our long-term, like-minded shareholders, who will benefit as their per share value continues to grow meaningfully over the coming years.

Since the third quarter of 2020, we have reduced adjusted net debt by approximately $137 million2, despite a $518 million increase related to the Apex Energy acquisition, and we continue to evaluate the timing of further debt reduction as part of our clinical capital allocation process. With the reductions in net debt, we extended our maturity runway, providing us with considerable flexibility to take advantage of any capital market disconnects or opportunities that may arise.

- As of December 31, 2025

- See Non-GAAP Measures